What Questions to Ask Before Buying a Home in a Charleston Flood Zone

What Questions to Ask Before Buying a Home in a Charleston Flood Zone

If you are buying a home in Charleston, SC and the property is in or near a flood zone, the questions you ask before making an offer can save you thousands of dollars and prevent serious regret. Leah Beaulieu and BJ Rodgers with Coast2Coast Properties walk buyers through flood zone due diligence on every transaction, and the checklist below covers what experienced buyers ask — and what first-timers often skip.

This is not about fear. Most Charleston flood zone homes are livable, insurable, and good investments. But the cost differences between a well-understood flood zone purchase and a poorly researched one can be significant. The time to ask these questions is before the offer, not after inspection.

The Short Answer

- Ask what FEMA flood zone the property is in (AE, X, VE, or other) and whether it has changed recently

- Request the elevation certificate — this is the single most important document for determining flood insurance cost

- Ask the seller what flood insurance currently costs and whether claims have been filed

- Ask whether the property itself has ever flooded, and ask about the road and surrounding area separately

- Find out if the home has been elevated and at what height relative to Base Flood Elevation (BFE)

- Ask whether a Letter of Map Amendment (LOMA) has been filed or if the zone designation is being contested

Question 1: What FEMA Flood Zone Is This Property In?

The starting point is the official FEMA flood zone designation. In the Charleston area, properties fall into several categories:

AE Zone: High-risk Special Flood Hazard Area (SFHA). The government calculates a 1% or greater annual chance of flooding. If you have a federally backed mortgage — FHA, VA, conventional — your lender will require flood insurance. These are the most common high-risk designations in downtown Charleston 29401, 29403, parts of West Ashley 29407, James Island 29412, and most coastal and waterfront neighborhoods.

VE Zone: Coastal high-hazard area. These are AE-equivalent zones with the added risk of wave action. More common on barrier islands like Isle of Palms 29451, Sullivan's Island 29482, and Folly Beach 29439. Flood insurance in VE zones is typically more expensive than AE.

X Zone (Shaded): Moderate risk — between 0.2% and 1% annual chance of flooding. Flood insurance is not required by most lenders but is often recommended. Many X-zone properties in Charleston still carry meaningful flood risk.

X Zone (Unshaded): Minimal flood risk per FEMA's current maps. No lender requirement for flood insurance, but this does not mean the property never floods.

Always verify the zone yourself at msc.fema.gov, not just by taking a seller's word for it. FEMA remaps periodically, and zone changes can happen without homeowners being fully aware.

Question 2: Is There an Elevation Certificate, and Can I See It?

The elevation certificate is the single most important document for a flood zone property purchase. It is a formal survey that records the home's lowest floor elevation relative to the Base Flood Elevation (BFE) for that location.

If a home sits above BFE, flood insurance is generally much cheaper. If it sits below BFE, flood insurance can be dramatically more expensive. The difference between one foot above and one foot below BFE can easily mean $1,000 to $4,000 or more per year in insurance costs, depending on the specific property.

For new construction or substantial improvements in a Special Flood Hazard Area, an elevation certificate is required by Charleston County and the City of Charleston. Many existing properties have them. If the current owner cannot produce one, you may need to commission one before closing — and what it shows will directly affect your insurance quote.

Leah Beaulieu and BJ Rodgers always advise buyers to get an insurance quote from a flood insurance specialist using the actual elevation certificate data before submitting an offer on an AE or VE zone property. The quote is free and takes the guesswork out of your budget.

Question 3: What Does Flood Insurance Currently Cost, and Who Is the Provider?

Ask for the current flood insurance policy, not just the annual premium number. The full policy tells you:

- Whether it is a National Flood Insurance Program (NFIP) policy or a private policy

- The coverage amounts for the structure and contents separately

- Whether there is a history of claims on the policy

- Whether the policy is assumable (some NFIP policies can transfer to a new buyer under certain conditions)

NFIP policies under FEMA's Risk Rating 2.0 system (rolled out in 2021-2022) are priced based on the property's specific risk rather than just its zone, so two homes in the same AE zone can have very different premiums. A property that qualifies for an assumable policy at a lower legacy rate can be a significant financial benefit — ask specifically about assumability.

If the current owner is carrying private flood insurance, ask why they chose private over NFIP and whether it has been renewed continuously. Gaps in flood insurance coverage can affect your ability to assume a policy.

Question 4: Has This Property Flooded? Has It Filed Flood Insurance Claims?

South Carolina law requires sellers to disclose known material defects, and flooding history is a material condition. Ask directly, in writing: has water entered the structure? Has the property filed any flood insurance claims?

You can also research NFIP claim history independently. FEMA maintains records of repetitive loss properties — homes that have filed two or more claims within ten years — and these are publicly searchable. A repetitive loss designation can significantly affect insurance costs and future insurability.

Ask about the house separately from the lot and the street. Some properties in Charleston have structures that have never taken water inside, but the lot floods regularly, the garage floods, or the street floods during king tides. All of these affect day-to-day livability and should be part of your due diligence.

Question 5: Has the Home Been Elevated, and What Is the Height Relative to BFE?

Elevated homes in Charleston AE zones sit on raised foundations — piers, posts, or fill — with the lowest habitable floor above Base Flood Elevation. The elevation certificate documents this. The higher above BFE, the lower the flood insurance premium typically will be.

Ask specifically:

- When was the home elevated, if it was elevated?

- What is the current elevation relative to BFE (in feet above or below)?

- Are there enclosures below the elevated floor, and are they flood-vented?

Enclosures below the elevated floor — garages, storage areas — must be properly flood-vented to qualify for lower insurance rates. Improper enclosures can void the benefit of elevation and trigger higher insurance costs. If the seller has added non-compliant improvements below the base flood elevation, that is a red flag.

Question 6: Has a Letter of Map Amendment (LOMA) Been Filed?

A Letter of Map Amendment (LOMA) is a formal FEMA determination that a specific property has been incorrectly included in a Special Flood Hazard Area based on the natural elevation of the land. If a home was placed in an AE flood zone because of its position on a FEMA map — not because of actual flood risk — a LOMA can remove it from the mandatory purchase requirement.

Ask the seller whether a LOMA has been filed and approved for the property. If it has, you may not be required to carry flood insurance even if the official map still shows the property in an AE zone. A LOMA approval from FEMA is the official documentation that enables this exemption.

If a LOMA has not been filed but the property sits at a high elevation relative to the mapped flood zone, BJ Rodgers and Leah Beaulieu recommend consulting with a licensed surveyor or floodplain manager before closing to evaluate whether a LOMA application makes sense.

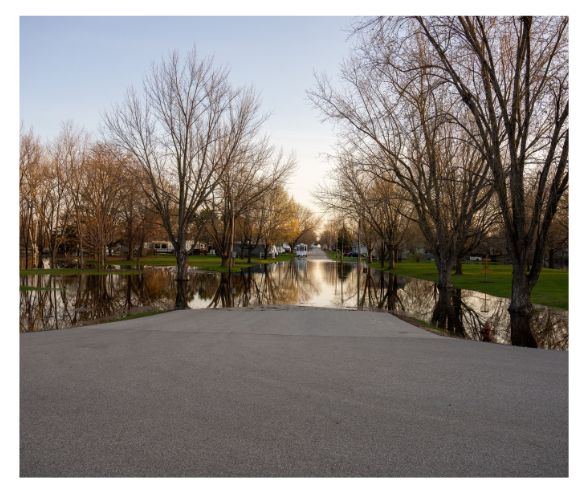

Question 7: What Happens to This Street During Heavy Rain and King Tides?

This question is separate from the property itself, and it is one buyers frequently forget to ask. In Charleston, the street flooding and access road conditions are separate from the home's flood zone designation.

Ask the seller:

- Does the street in front of the home flood during heavy rain?

- How often is it impassable during king tide events in fall?

- Is there an alternate access route?

Use the City of Charleston's TIDEeye tool (gis.charleston-sc.gov/tideeye/) to look up the specific street's tidal flood history. Drive by the property after a heavy rain. Check with neighbors if possible.

A home on the lower peninsula of downtown Charleston 29401 or 29403 may have excellent elevation and reasonable flood insurance, but sit on a street that closes several times per year during tidal flooding. That commute and lifestyle impact is real and should factor into your decision.

Question 8: What Are the Flood Zone Conditions in the Broader Neighborhood I'm Considering?

Individual property questions are necessary but not sufficient. It also helps to understand the flood profile of the neighborhood broadly.

Properties in Summerville 29483 and 29485, Goose Creek 29445, and inland North Charleston 29406 are largely in X zones and have limited tidal flood exposure. Buyers who want to minimize flood zone complexity should weight these areas accordingly.

Properties in downtown Charleston 29401 and 29403, James Island 29412 near the water, Mount Pleasant 29464 close to the harbor, and barrier islands carry more flood zone complexity. That does not make them bad purchases, but it does mean the due diligence steps above matter more.

The Biggest Mistake Buyers Make in Charleston Flood Zones

The biggest mistake is getting a flood insurance quote only after the offer is accepted — or worse, after inspection. By that point, buyers have emotional investment in the property and are less likely to walk away even if the insurance cost is significantly higher than expected.

The right sequence is: get the elevation certificate before the offer, run a flood insurance quote from a licensed flood insurance specialist using that certificate, include the annual flood insurance cost in your total monthly housing budget, and only then decide on your offer price.

A second mistake: relying on the current owner's insurance premium without checking current Risk Rating 2.0 pricing. FEMA's rate methodology changed in 2021-2022, and a policy that was renewed without interruption may be grandfathered at a lower rate that will not transfer to a new buyer. The new owner's premium could be significantly different from what the seller currently pays.

A Realistic Example

A buyer relocating from Atlanta to Mount Pleasant 29464 finds a beautiful home in an AE zone close to the waterfront. The seller mentions flood insurance runs about $1,800 per year. The buyer checks the box in their head and moves forward.

After the offer is accepted and inspection is complete, they finally get a formal flood insurance quote using the elevation certificate — and discover the home sits 1.5 feet below Base Flood Elevation. Their new policy under Risk Rating 2.0 will run $3,800 per year, not $1,800. The difference is $2,000 per year, or about $167 per month. That changes the affordability calculation materially.

Because they asked this question at inspection rather than before the offer, they are now in a tougher negotiating position. They end up negotiating a modest price reduction, but the deal would have looked different — and the price they offered would have been lower — if they had the accurate insurance number earlier.

Summary: Questions to Ask Before Buying in a Charleston Flood Zone

- What FEMA zone is the property in — AE, VE, shaded X, or unshaded X?

- Is there an elevation certificate, and what is the home's elevation relative to BFE?

- What does flood insurance currently cost, and is the policy assumable?

- Has the property flooded, and have any claims been filed with NFIP?

- Has the home been elevated, and are any below-floor enclosures properly vented?

- Has a Letter of Map Amendment been filed?

- Does the street flood during heavy rain or king tides?

- What is the broader flood profile of the neighborhood I'm considering?

FAQ

Do I have to buy flood insurance if I'm buying in an AE flood zone in Charleston?

If you have a federally backed mortgage — FHA, VA, conventional — your lender will require flood insurance on any property in a FEMA Special Flood Hazard Area (AE or VE zones). If you are buying with cash, you are not legally required to carry it, but it is strongly advisable given the real risk and the potential for significant losses.

What is an elevation certificate and why does it matter?

An elevation certificate is a professional survey documenting where the home's lowest floor sits relative to the Base Flood Elevation for that location. It is the primary document used to price flood insurance. A home above BFE typically has much lower premiums than one below BFE — sometimes by thousands of dollars annually.

Can I assume the seller's flood insurance policy?

Some NFIP policies are assumable under specific conditions. You would need to apply to assume the policy and meet NFIP requirements. Private flood insurance policies are generally not assumable. Ask your insurance agent and the seller's agent to verify assumability during the due diligence period.

What is a repetitive loss property and why should I care?

A repetitive loss property is one that has filed two or more NFIP claims within ten years. These properties may face surcharges on future NFIP policies and may have difficulty obtaining coverage. FEMA's public records can reveal repetitive loss status for a property, which is important information before buying.

What is FEMA Risk Rating 2.0 and how does it affect flood insurance costs?

Risk Rating 2.0 is FEMA's updated flood insurance pricing methodology, rolled out 2021-2022. It calculates premiums based on the specific property's risk factors — including structure type, elevation, distance to water, and more — rather than just flood zone. The result is that some properties pay more than before, some less. New buyers receive Risk Rating 2.0 pricing; existing policyholders may be grandfathered at different rates. Always get a new quote rather than assuming the seller's premium applies to you.

What is the difference between flood insurance and homeowner's insurance for Charleston properties?

Standard homeowner's insurance does not cover flooding. Flood damage — water entering from outside the structure due to tidal surge, river overflow, rain runoff — is covered by a separate flood insurance policy, either through NFIP or private insurers. In AE and VE zones, you need both policies. The homeowner's policy covers wind damage, fire, and other perils; the flood policy covers flood losses specifically.

How do I find out if a Charleston property's street floods regularly?

Use the City of Charleston's TIDEeye tool at gis.charleston-sc.gov/tideeye/ to look up tidal flood history and forecasts for specific streets. Also ask the seller directly, check with neighbors, and visit the property after a heavy rain if possible.

Final Answer

Buying in a Charleston flood zone is a manageable, often worthwhile decision — but it requires asking specific questions before the offer, not after. The most important steps are getting the elevation certificate early, running a real flood insurance quote using that data, asking directly about flooding history and claims, and checking street conditions separately from the home itself.

Leah Beaulieu and BJ Rodgers with Coast2Coast Properties guide buyers through this exact process on every flood zone transaction in the Charleston area. Whether you are looking at waterfront properties in Mount Pleasant 29464, historic homes downtown in 29401, or comparing flood risk across neighborhoods, the right due diligence makes the difference between a purchase you understand fully and one that surprises you later.

About Leah Beaulieu & BJ Rodgers — Coast2Coast Properties

Leah Beaulieu and BJ Rodgers are Charleston, South Carolina real estate professionals with Coast2Coast Properties, helping buyers compare neighborhoods, understand local market differences, and find the right fit across the Charleston area. Whether you are buying your first home, relocating to the Lowcountry, or looking for investment opportunities, Leah and BJ bring local knowledge, straight talk, and a genuine commitment to helping clients make smart decisions.

Coast2Coast Properties

www.coast2coastprop.com

843-697-1409 / 803-201-4259